Egypt and Gulf yards as strategic hubs for a Northern Sea Route?

From sand to snow

Can Egypt and Gulf yards act as Arctic strategic hubs, asks Ahmed Ghowel, PhD, MRINA, IEng, PMP, who brings 20 years of shipyard experience across the MENA region and North America.

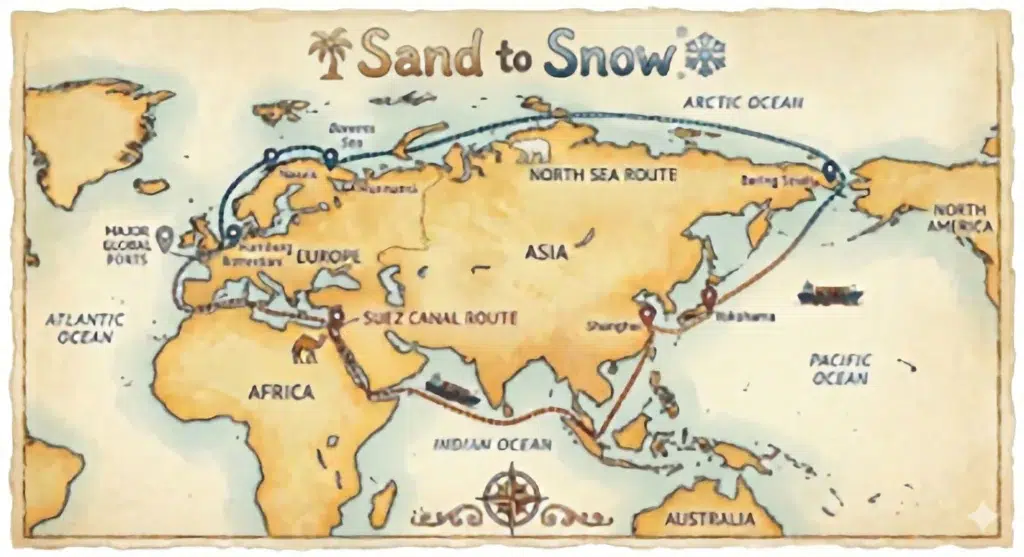

As Arctic sea ice retreats, the Northern Sea Route (NSR) is consolidating its position as a strategically significant complement to traditional east-west shipping corridors. The 5,600km passage along Russia’s northern coastline shortens the sailing distance between Northern Europe and East Asia by around 40% relative to the Suez Canal, with associated reductions in transit time and fuel consumption that can more than double operational energy efficiency under favourable conditions (Schøyen & Bråthen, 2011; Husdal, 2011). Cargo volumes, while still modest in global terms, increased from roughly 34 million tons in 2022 to 36.2 million tons in 2023, signalling growing commercial interest in this emerging corridor (Arctic Review, 2023). For the Middle East, a region historically defined by deserts, hydrocarbons and warm‑water chokepoints, this development presents not only a routing alternative but also a strategic opportunity to reposition itself as a provider of critical capabilities to the polar maritime economy.

Northern Sea Route-Suez studies

Seminal work by Schøyen and Bråthen (2011) offers a detailed comparative analysis of the Northern Sea Route and the Suez Canal Route (SCR) using two bulk shipping cases on Norway-China trades. Their voyage‑level assessment quantifies differences in distance, sailing days, operating costs and energy efficiency across Northern Sea Route, Suez and Cape of Good Hope alternatives, demonstrating that the Northern Sea Route can reduce distance by approximately 40% and more than double operational energy efficiency when navigable.

The present analysis builds on these insights but shifts the analytical lens in three important ways. First, whereas Schøyen and Bråthen focus on voyage economics and route competitiveness, we foreground the capability geography underlying Northern Sea Route-Suez utilisation by examining how Middle Eastern and Egyptian human capital, shipbuilding and repair infrastructure and operational expertise enable or constrain the practical uptake of Arctic routes (Schøyen & Bråthen, 2011; Zeng et al., 2020). Second, while their framework largely treats the Northern Sea Route and Suez as alternative corridors to be compared, we conceptualise them as components of an integrated, seasonally adaptive Suez-NSR network in which hybrid routing can generate resilience and emissions benefits, particularly in light of recent disruptions in the Red Sea and Eastern Mediterranean (BiznesAlert, 2021; RiverBasin, 2024). Third, we introduce the Middle East and Egypt as under‑examined but increasingly central actors in Arctic shipping, arguing that Gulf universities, Egyptian maritime institutions and shipyards along the Suez Canal are emerging as key providers of design, maintenance and governance capabilities for polar‑capable fleets ̶ a dimension largely absent from existing NSR-Suez cost‑comparison models (New Maritime Trade Routes, 2019; Zeng et al., 2020).

In doing so, this analysis complements route‑level economic analyses by asking not only whether the Northern Sea Route is competitive, but who is building the technical, institutional and infrastructural capacity to operationalise and govern an emerging NSR-Suez system over the coming decades.

The 5,600km passage along Russia’s northern coastline shortens the sailing distance between Northern Europe and East Asia by around 40% relative to the Suez Canal

Human capital as a strategic differentiator

A core argument is that the Middle East’s emerging role in Arctic shipping is underpinned less by geography and more by deliberate investments in specialised human capital. While prior Northern Sea Route studies emphasise distance savings, cost structures and environmental performance, they pay limited attention to where the engineering, operational and maintenance expertise required for safe polar navigation will be produced and anchored (Schøyen & Bråthen, 2011; Husdal, 2011; Zeng et al., 2020). This analysis addresses that gap by foregrounding Gulf states and Egypt as producers, rather than merely users, of Arctic shipping technology and know-how, particularly as Arctic nations grapple with acute skilled workforce shortages amid rising shipping demands.

Arctic shipping traffic hit a record 1,812 unique ships in the Polar Code area in 2025, up 40% since 2013, driven by resource extraction, yet key nations face severe labour gaps in maritime expertise. Canada’s marine sector reported over 3,600 unfilled seafaring positions in 2024 (11% vacancy rate, triple the national average) and needs 8,300 new workers by 2029 ̶ 30% of its current workforce ̶ with training institutions covering only 40% of demand. Globally, officer shortages stand at 8.5% today, projected to hit 10% by 2030 due to fleet growth and retirements, while Denmark’s maritime industry has near-zero unemployment for specialists, forcing reliance on foreign talent.

Universities across the Gulf Cooperation Council ̶ including Khalifa University in the United Arab Emirates, Qatar University and King Fahd University of Petroleum and Minerals in Saudi Arabia ̶ have developed programmes that explicitly target polar and extreme-environment challenges, with curricula in ice-class hull design, advanced computational hydrodynamics, and cryogenic systems. These initiatives effectively repurpose desert-born engineering ecosystems to address high-latitude operational risks, potentially filling Arctic gaps through joint academic programmes and internships. In parallel, Egypt’s well-established maritime institutions, notably Alexandria University, Port Said University and Arab Academy for Science, Technology & Maritime Transport (AASTMT), provide expertise in ship design, offshore structures, canal operations and port management, creating a cross-regional talent pipeline that spans both Arctic technology and warm-water chokepoints; targeted internships could channel this into Arctic needs, building on Middle East shipbuilding’s potential for 50,000-70,000 new jobs.

The impact of this human-capital strategy is visible in global classification and design activities. Alumni from regional centres of excellence, such as offshore research programmes at King Fahd University, have contributed to polar notation standards at the American Bureau of Shipping, while Middle Eastern naval architects participate in the design of double-acting tankers and other ice-strengthened vessels capable of efficient operation in both ice-covered and open-water conditions (UNCTAD, 2023; Schøyen & Bråthen, 2011). Their comparative advantage lies in transferring experience from hot, high-salinity, high-wave-energy Gulf environments to robust design solutions for minus-50-degree Arctic gales. Recent UNCTAD and industry analyses underscore the region’s growing share of maritime R&D talent and forecast substantial expansion of the skilled maritime workforce by 2030, reinforcing the scale of this human-capital pivot (UNCTAD, 2023).

The Suez-Northern Sea Route nexus as a networked architecture

Existing scholarship has convincingly shown that the Northern Sea Route offers distance and emissions advantages but is constrained by seasonality, schedule unreliability and high ice‑class capital costs (Schøyen & Bråthen, 2011; Husdal, 2011; Zeng et al., 2020). Studies such as Schøyen and Bråthen’s conclude that, despite its theoretical efficiency, the NSR is currently most attractive for certain bulk trades and remains ill‑suited to high‑frequency container services (Schøyen & Bråthen, 2011). Much of this literature frames the Northern Sea Route and Suez in binary terms, treating them as competing substitutes and emphasising potential risks to Suez Canal revenues under high Northern Sea Route‑uptake scenarios (Khan, 2015; BiznesAlert, 2021).

This analysis advances the debate by reframing the relationship as a networked architecture rather than a zero‑sum competition. In practice, the Suez Canal remains a high‑throughput, year‑round artery carrying roughly 12% of global trade and functioning as the Mediterranean gateway for Asia-Europe flows (Valdai Club, 2018; Arctic Review, 2023). At the same time, hybrid routing concepts ̶ such as a Rotterdam-Yokohama loop combining NSR segments with Suez transits ̶ can generate operational synergies, including voyage time reductions in the order of two weeks and significant CO2 abatement per round trip, as highlighted in European maritime risk and safety assessments (Arctic Review, 2023; Zeng et al., 2020).

Within this networked view, Middle Eastern and Egyptian actors are not passive price‑takers but system integrators.

Egyptian shipyards as polar‑capable hubs

Most Northern Sea Route analyses concentrate on Northern European and East Asian shipbuilding and repair clusters, paying limited attention to shipyard capacity along the Suez corridor (New Maritime Trade Routes, 2019; FNI, 2000). This analysis instead foregrounds Egyptian shipyards as strategically located assets in the emerging Arctic maintenance and retrofit landscape. Major facilities distributed along the Suez Canal ̶ Shipyard, Port Said Shipyard, Port Tawfik Shipyard, Suez Shipyard and Canal Naval Constructions in Port Fouad ̶ offer substantial dry dock capacity, floating docks and repair berths for a wide range of vessel sizes. Their positions at the northern and southern entrances to the Canal make them natural service nodes for ships transitioning between Northern Sea Route segments and conventional East-West legs.

As forecasts suggest that a growing portion of the global fleet will be ice‑strengthened or partially polar‑capable by 2030, these yards are well placed to compete for retrofit, maintenance and life‑extension work on ice‑class tonnage. Their existing heavy‑steel repair capability, coupled with modernisation programmes and proximity to major traffic flows, enable them to specialise in hull reinforcement, low‑temperature steel welding and winterisation systems. Furthermore, their tight coupling with Egypt’s maritime universities ensures a steady supply of engineers and technicians who understand both the operational constraints of canal transit and the technical requirements of polar vessel maintenance. This positions Egypt not only as a transit state but as a service and knowledge hub within the broader Arctic shipping ecosystem.

More articles like this can be found in the latest issue of DryDock magazine